The architects of our post war civilization suffered greatly for their knowledge. Having watched Europe stumble blind into disaster in 1914, blundering on to genocide thirty years latter these policy makers earned in blood and toil a terrible respect for the Vulcan power inherent in the industrial systems they managed, power for both good and evil that all too easily grinds individuals to dust. Even before the outcome was clear, in the thick of World War II these humanists began to lay the groundwork for what would become the most successful framework of political economy in human history, a framework that would take the world from 2.5 to 7 billion souls who live both longer and better.

The burden of such success is pressure each of us now bears to exceed the standards set by our predecessors. Occasionally epochs consume their paradigm and having done so raise this pressure logarithmically. When success outstrips the basic conditions that spawn it and progress stalls before what is old has finally collapsed, with the new defenseless in utero, the resulting hiatus is a limbo where both grand vision and epic execution are required just to maintain the achievements of the expiring era. To even imagine a future, something fundamentally new must be conjured into being. This is what we are living through. As the Homogenocene extinguishes species at a pace to rival the Cretaceous asteroid impact, our voiceless dominions in other genomes are expressing their disapproval by simply vanishing. The narcissistic cacophony of our politics drowns their growing silence as we shout down even the distressed humanity who bear in hardship the shortcomings of our aging and overtaxed systems at who's margins it is increasingly difficult even for people to survive.

Until his death in 1946, J. M. Keynes, a visionary even among that heroic generation of institution builders, had been struggling against the US to implement a global commercial system that would mechanically balance trade and financial flows by requiring both surplus and deficit nations to engage in mutually re-balancing adjustments. It is a tribute to both the quality of the system he helped to build and his insight into what would be its failure that while his institutions prevailed with astronomical success for thirty years, as they decayed over the following forty they ultimately failed on exactly the issues with which he struggled as he died: imbalances of trade and the persistence of an ideology that placed hard money over soft humanity.

As he understood, money is a tool to engage humanity in making our world a better place, a tool of almost unlimited and hard power who's material creations can sparkle so promiscuously as to occlude the soft human utility that is in reality its only value: it is we who grant money value, not the other way around. When money distracts us from our own centrality to the question of value, it turns us against ourselves by poisoning relations between us, blinding us to our own centrality in a viciousness well understood thousands of years ago when an Israelite said to his friend Paul "the love of money is the root of all evil ".

As he understood, money is a tool to engage humanity in making our world a better place, a tool of almost unlimited and hard power who's material creations can sparkle so promiscuously as to occlude the soft human utility that is in reality its only value: it is we who grant money value, not the other way around. When money distracts us from our own centrality to the question of value, it turns us against ourselves by poisoning relations between us, blinding us to our own centrality in a viciousness well understood thousands of years ago when an Israelite said to his friend Paul "the love of money is the root of all evil ".

Keynes compromised system of commerce was put into effect in the closing years of the Second World War and despite its defects saw to it that all people engaged in its functions were both put to use and benefited personally from what use to which they had been put. It was a system that placed human well-being at the center of its values, rightly ranking money subsidiary. While a tool of great potential benefit, money was none the less of secondary importance, no more than a tool to be deployed for the good of humanity at large. This system supported the re-construction of Europe and Japan, the prosperity and growth of the United States and a general growth in health and longevity world-wide. It was an era unprecedented in history. But markets distribute and power concentrates, and after thirty years concentration power began to distort the distribution of markets to the benefit of the corporations Eisenhower had warned about in his valedictory as "the military industrial complex".

Vertically integrated monopolistic corporations in energy, agriculture, munitions, logistics and communications, corporations deeply identified with the US government began to steer policy toward their own ambitions. These private interests, to juice their returns, encouraged the excesses of the Cold War in South East Asia, the Middle East, and South America generating imbalances that began to subvert Keynes' Breton Woods currency regime, a hard money kludge American Bankers had insisted on in place of his design for system of mutually balancing adjustments of global trade.

War consumption for Viet Nam combined with the domestic spending of Great Society programs to overwhelm the US industrial base and draw in imports converting us from a net surplus to net debtor economy, first and primarily for the import of oil. The foreign exchange pressures of this shift pushed Nixon to finally abandon the Breton Woods currency pegs and with them gold backing of the dollar. Viewed as a default on promised gold for oil by our suppliers this (along with our military alignment with Israel) lead directly to the formation of the cartel of Oil Producing and Exporting Countries (OPEC).

{kind=link}

OPECs' oil embargo was blow back to obtuse US monetary, energy and military policies. It converted a latent inflation into an actual one that had been immanent for some time in the sustained over consumption of real resources for both social policy and war. When the oil embargoes pushed input costs up across the energy intensive US economy our defacto industrial policy was cast into high relief:

In 1971 future Supreme Court Justice Lewis Powell wrote his infamous memo calling on corporations to become more active in politics. Corporations rose to the occasion funding "think tanks", "media" and "educational" programs that have persistently tilted both our electoral politics and our judiciary toward the interests of these business entities and re-framed the role of government as the protector of profits rather than people. Among the fruits of this effort were creations like the Koch mouthpiece CATO Institute that funds "research" (propaganda) on its anarcho-corporatist libertarian ideal, or the consolidation of Rupert Murdoch's media empire as a 24/7 anti US voice, wrapping infantile selfishness in the flag, or the founding of the Federalist Society at Yale to "educate" (indoctrinate) legal scholars and students in the legal underpinnings and definitional legerdemain of corporatism necessary to understanding people as the implements of wealth rather than the other way around.

Parallel to this external corporatist challenge mounted against the constraints The United States had placed on business activity, within the government itself a complementary line of attack was being mounted by Milton Friedman, Alan Greenspan and their administrative minions who would play central roles in the second and third Bush Presidencies. The ideas and political influence of this coterie would do more to redirect the priorities of government than all the private sector corporatist efforts combined. Their ideas ennobled corporations and particularly corporate managements. At the same time, they denigrated essential government regulatory institutions, degraded "labor" as the sole cause of inflation and re-conceptualized citizens as "consumers".

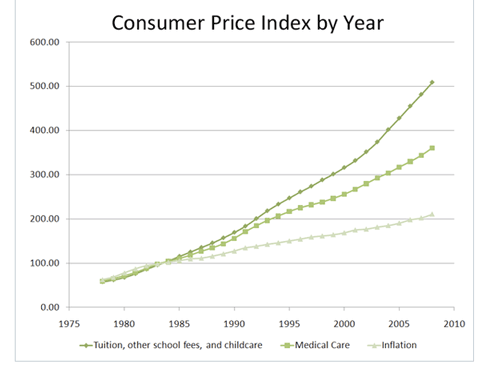

Friedman began by perverting Abba Lerner's theory of high and low full employment to include only low full employment, entirely abandoning any notion of high and low and the essential realities of the Great Depression that had conjured Lerner’s insight into existence in the first place. This stood the very idea of full employment on its head, perverting it to justify using the unemployed as a buffer stock to control inflation. This was packaged with a bunch of math and called NAIRU (1975), the Non Accelerating Inflation Rate of Unemployment. The wage price spiral that erupted after the OPEC shocks lent political cover to what was a bald grab of the income stream that had gone to labor as a result of its productivity growth as a key component of the New Deal. This would in a stroke divorce wage growth from efficiency growth for the next forty years and lead to both the asset bubble and demand collapse with which we tenuously live today.

{kind=link}

Alan Greenspan had a more robustly devastating career. First he would convince the Carter administration to stand antitrust enforcement on its head by "enforcing" for "efficiency" rather than against industry consolidation. Arguing that consolidation was good so long as monopoly power was used to drive consumer prices down rather than profit margins up, two generations of upside down anti-trust non-enforcement has left every significant sector of the US economy in some form of monopolistic organization with all the expected restraint on competition and depression of job creation this implies. Rewarding this early success for the corporatist agenda, Reagan appointed Greenspan Chairman of the Federal Reserve.

As Chairman of the Fed, Greenspan would spend most of the next twenty years using NAIRU to suppress the income growth of wage earners despite their accelerating productivity gains. At the same time he encouraged the beneficiaries of the diversion of income from wages to capital to loan those gains back to the workers who properly had earned them. This converted historical productivity growth by workers into a rent paid to capital by the very earners who should have seen these gains as private income: it converted earned income by working Americans into rents paid to corporations. Greenspan's permanently low interest rates concealed until shortly after his retirement the debt penury into which this sleight of hand had pressed a great many Americans.

{kind=link}

This Neo-Liberal ascent to power, conceived by Powell, Friedman and Greenspan, among a caucus of corporate managements and magnates, was executed by presidents Ford, Carter, Reagan, Clinton, Bush and now Obama. It reached its apotheosis with the Citizens United ruling, the final payoff of corporate investment in legal indoctrination, just last year (the history of the doctrine of corporate personhood is both shocking and disgusting). Both Democrats and Republicans, with the notable exception of George Herbert Walker Bush (in this particular an honorable throwback to the democratic capitalism of the New Deal), have encouraged and accelerated an upward re-distribution of wealth. This has been the defining but fastidiously unstated central goal of the Neo-Liberal era: it has left fewer and fewer free to shape markets more and more through the power of their concentrated wealth.

Wage earners for two generation have lived with stagnating wages, products of NAIRU and the monopolistic suppression of job creation. At the same time their main assets (homes), investments (education) and risks (health care) have all become considerably more expensive . These divergent pressures, increasing costs with flat incomes, have combined with the Greenspan Put (excessively low interest rates that concealed the problem until the bubble burst) to draw ever deeper into debt an ever broader pool of the very wage earners who's productivity gains these policies have invisibly handed to "investors". The bubble that remains in markets outside of housing, primarily in financial assets, is in fact the mirror image of the debt burden of most working Americans. The Neo-Liberal ideology that insists that everything will work out if we just make the rich richer and the poor poorer has foundered on the shoals of mass unemployment and its own sustained failure to have anything useful to say on issues facing the real economy. Meanwhile Neo-Liberalism's ultimate dupe or enabler, our supposedly liberal President, keeps imploring the plutocrats to lend their hoards as if there remain working Americans who want more debt and anyone could imagine them having the income to pay it back in future.

{kind=link}

For the Neo-Liberal faithful "the love of money" is a golden mirror in which the reflection of their greed is absolute virtue. In this gilded reflection all who've failed to acquire the wealth to weather Neo-Classical economics' inevitable deflations are revealed as the immoral creatures their impoverished state proves them to be (Neo-Classical economics put the Neo- in Neo-Liberalism). This money obsession, among those who control its flows, ravages societies when the insistence on the preservation of money value depletes precisely the flows that are essential in the lives of the modern industrialized poor.

Robbed of recourse to the fruits of the land by urbanization, for the contemporary poor the distributive property of money, its ability to connect supply with demand, is the only real value it actually has. Stoppages in its flow at the base of modern economies leave broad swaths of the population hungry and homeless. A quasi religious belief that government expenditures not mated to bond sales will induce hyper-inflation is used to justify imposing these stark and potentially lethal hardships on the poor, cutting jobs and cutting income while insisting that debts be honored. The poor are wrung out like sponges to moisten the liquidity of financial gamblers who actually created the deflationary financial shock in the first place.

Robbed of recourse to the fruits of the land by urbanization, for the contemporary poor the distributive property of money, its ability to connect supply with demand, is the only real value it actually has. Stoppages in its flow at the base of modern economies leave broad swaths of the population hungry and homeless. A quasi religious belief that government expenditures not mated to bond sales will induce hyper-inflation is used to justify imposing these stark and potentially lethal hardships on the poor, cutting jobs and cutting income while insisting that debts be honored. The poor are wrung out like sponges to moisten the liquidity of financial gamblers who actually created the deflationary financial shock in the first place.

The deflationary ideology of Neo-Liberalism infects societies that host it and ravages them at regular intervals like malaria. We see its cyclical fever breaks repeating in the Euro Zone these last four years as Iceland, then Ireland, Spain, Greece, Italy and then again Spain have all succumbed to the cold sweats of deflation, only to be hectored by their betters for the sin of their suffering and treated with leeches. Now Belgium, France and Germany have had their first blushes of heat. Each time, like priests repeating a catechism, we hear from the "Troika" (bank bureaucrats who in what appears to be a financial coup de etat now run the Euro Zone through the ECB) how the flow of funds to people who depend on them for subsistence must be now visibly handed over to the service of debts who's very existence is all the evidence required to condemn those misguided souls of "profligacy", the worst moral bankruptcy of the Neo-Liberal liturgy. This is how power makes the invisible hand visible and prevents markets from distributing. This is a very real abridgement of freedom for the unemployed in these societies who did not choose their condition but deal with the most brutal consequences of a systemic failure while the extraction machine that actually created the debts in the first place continues unaltered.

The malarial spore is killing its host. Over a generation ago having lost any contact with the real economy of income and expenditure, from and for the real things that make life worth living, Neo-Liberal ideologues have convinced themselves of an ecstatic vision they call "expansionary contraction". In this hallucination the reduction of the stock of financial assets somehow causes future demand formation so acute today's investors will rush to deploy what's left of their wealth toward it in fits of expansionary investment. No evidence has ever been shown to support this belief, but the faith persists. Despite the multi trillion stockpiles of corporate cash currently hoarded on both shores of the Atlantic, pining for the opportunity to invest when some perceptible future demand begins to shimmer on some horizon, Troika grandees insist that if only the working people of Europe are reduced to a suitable desperation, demand will magically conjure investment opportunities into existence and all will right itself. Where actual cash to express such demand will come from is simply left to faith.

{kind=link}

There is no alternative we are told because any spending by governments will only add to the debt and increase the likelihood of default by driving interest rates up. But the only force pushing European states toward default and European interest rates up is the fatally flawed construction of their fiscal union. The US, the UK, Japan and Canada, as they deficit spend, experience interest rates decline: they are monetarily sovereign issuers of their own floating fiat currencies. They actually issue the money they spend, they make it and, of essential importance, they denominate all of their national debts in it. The Euro countries are users of the Euro, not issuers of it. The issuer of the Euro is the un-elected creation of a set of convoluted treaties, the European Central Bank (ECB). It answers to no one in anything like a democratic or representative way. Its legitimacy rests on the statesmen who created it against the wishes of or with the great reservations of their countrymen. This bank apparently only considers the interests of creditors of relevance and seems to view those interests as well beyond mere relevance, as somehow sacred. It wants the citizens who use the currency to somehow honor their debts even as their income, employment and public benefits, all opportunity to acquire the currency, are withheld. The historical obligations of nations to their people seem to be of no interest whatsoever to the ECB which appears to imagine that Europeans will somehow conjure money from thin air to honor their Euro denominated debts. The ECB could solve this problem today and affect a solution within months by funding national investment programs to put income into the hands of European workers who want to pay their bills but can’t in the environment of austerity the ECB has bullied national governments to implement and enforced through threats of bankrupting recalcitrants like Greece where elected leaders had the temerity to propose a referendum on the subject, an actual act of democratic governance.

In the US, the UK, in Canada and Japan, as national debt has gone up, the interest rates these monetarily sovereign nations pay has gone down. This is a mechanical effect of deficit spending in monetarily sovereign states with floating fiat currencies and debts denominated in their own currencies. This is a testable and proven fact that Neo-Liberal economics scrupulously refuses to recognize elaborating ever more absurd Rube Goldberg contraptions to conceal. Like religious authorities insisting the sun revolves around the earth they insist through the propaganda organs they control what is demonstrably false and threaten with eternal damnation anyone who looks for evidence of this fact.

The reality of monetary sovereignty is no less applicable to the Euro zone, except that the zone was set up by the faithful specifically to deny it. The German obsession with the Wiemar hyperinflation, completely misunderstanding the causality of that event, a politically induced calamity that was reversed in a matter of weeks when the policies that created it were reversed, led to the construction of a European monetary system guaranteed to induce deflation in the first systemic setback that happened to correlate across borders. The ECB obsession with the preservation both of currency value and the capital stocks stored in sovereign debt is in fact encouraging the destruction of exactly those capital stocks: deflationary pressure is everywhere in evidence and the ECB girds its loins for a death match with phantom inflation.

It is far more likely that these capital stocks will be depleted through managers "performance" bonuses, rewarding themselves for stock buy-backs or other non-productive financial engineering, or obliterated by the financial apocalypse looming in Euro Zone deflation which these same managements are assiduously looting ahead of, expatriating their booty to Germany, Switzerland of the UK before it vanishes. And even as they spiral up to the event horizon of monetary doom, they insist that if only the poor could be made poorer the disaster could be averted. It is "the love of money" that blinds both the Troika and America's deficit hysterics to the obvious, available and tested solutions to these problems. Solutions that leave all the wealth thus far concentrated concentrated exactly where it is in the hands of the Neo-Liberal ordained, solutions that would save them too, save them from themselves. But these solutions can not be countenanced within the Neo-Liberal church of mammon because they will inevitably impose a relative decline in the monetary value of the asset concentrations currently being hoarded, hoards at risk of self extinguishment in a debt deflation they are in fact both the symptom and the cause of.

Part 2

Part 2

No comments:

Post a Comment